CLIMATE. MONEY. WORK. PODCAST | EPISODE 2

Woke ESG: What ESG investing is and isn’t

Guest: Blythe Clark, ESG Global Advisors

How do we actually define ESG investing? In March, 21 Republican attorneys general expressed their concerns around ESG to 53 of the largest fund firms, arguing that their focus on ESG is not in line with their clients’ financial interests.

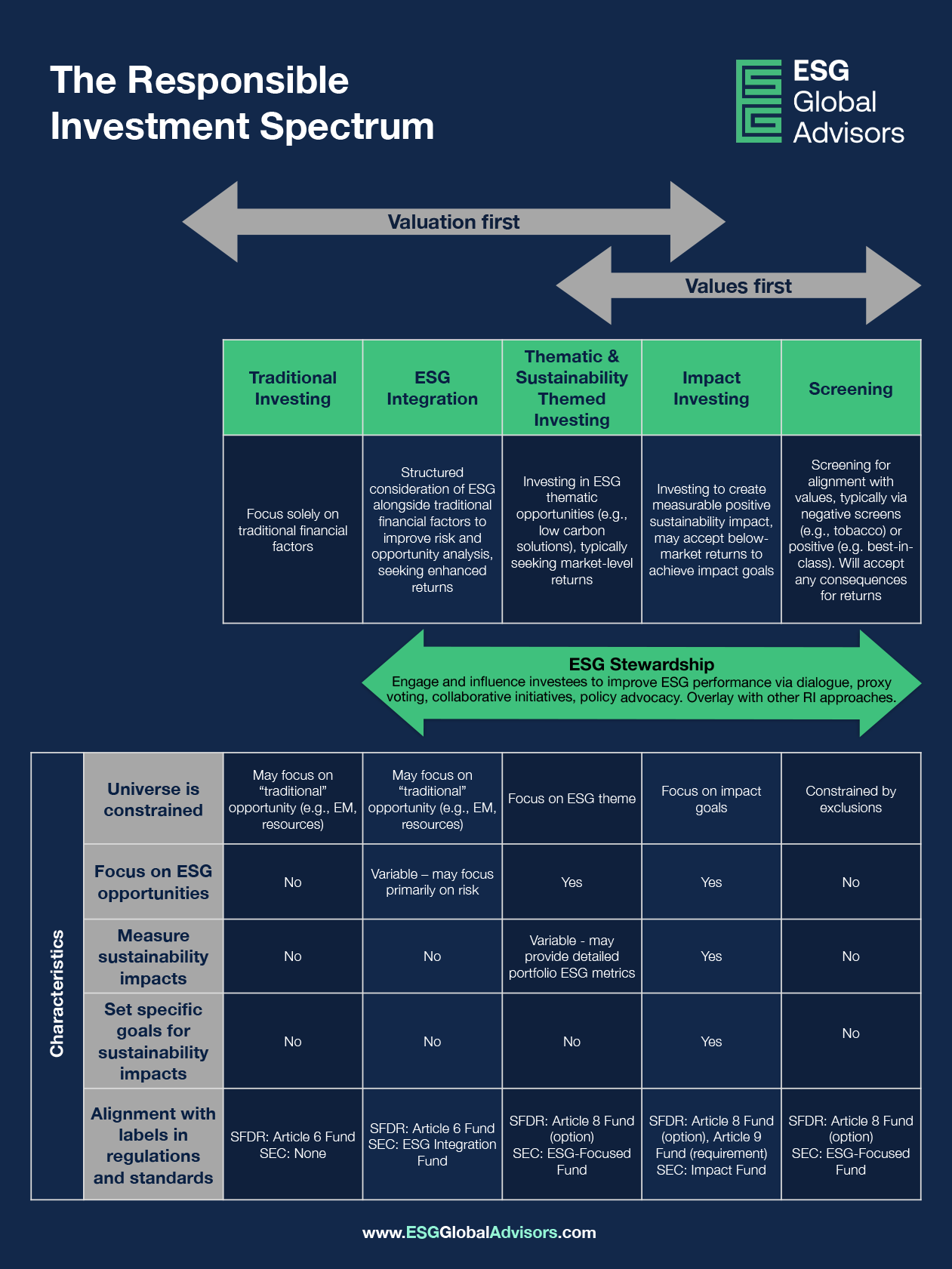

At the center of the debate is a focus on what ESG investing is, what it is not, and the role of risk. To unpack all of this, we sat down with Blythe Clark, director at ESG Global Advisors. She explains why it’s essential to differentiate between values and valuation, and gives an overview of why, when viewed through the lens of financial materiality, ESG investing is consistent with fiduciary duty. Plus, she and Keesa discuss a fantastic chart (link below) that ESG Global Advisors has to explain the different types of ESG investing.

View ESG Global Advisors’ Responsible Investment Spectrum chart here.

{kind=link}

Follow: Spotify / Apple Podcasts / Google Podcasts / YouTube / More

Transcript

Keesa Schreane:

Woke ESG. It's still trending. Yep, it's still a thing. And the debate is heating up. And at the center of it, there is a focus on what ESG investing is, what it is not, and the role of risk. So here with more detail about ESG investing variations and the role of risk is Blythe Clark, director at ESG Global Advisors. Now, ESG Global Advisors provides consulting services to companies and investors around responsible investing, educating, capacity building, benchmarking analysis, as well as research and rating analysis. Blythe, welcome.

Blythe Clark:

Thanks, Keesa. It's great to be here.

Keesa Schreane:

Great. So I really want to dive into the so-called woke ESG movement, it's been around for a while now, and how ESG investing is really defined. And we're going to get to that, but first, give us some clear use cases around how ESG Global Advisors, how they work with their clients, corporate clients, investors? And what are the objectives, and what does success look like?

Blythe Clark:

Well, as a boutique ESG consultancy, we are passionate pragmatists, and we believe that incremental changes have an exponential impact over time. And thus we seek to give clear objective recommendations, but do not seek to impose a predetermined ESG approach on our clients. We benefit from having a multidisciplinary team, with experts in institutional investment, corporate governance and engagement, environmental science, sustainability, accounting and reporting. And most of our growth, as a testament to, I think, the quality of our work, has come from existing clients. So either new work or referrals.

Keesa Schreane:

So talk about a success story. And obviously we can leave the name, etc., anonymous. But when you go into a consultation, what are your success metrics, and what does success look like? What have you done in terms of output that made you say, "Hey, this was a great engagement"?

Blythe Clark:

Client satisfaction. I think meeting a client where they are at and helping them to achieve their level of ambition. As part of our capacity building services within responsible investment, we'll consider where a client's current practices are and what their level of ambition is. And at the end of engagement, we look at, "Have we helped the client achieve the level of ambition they set out when engaging in capacity building?"

Keesa Schreane:

So what have you seen in terms of clients who are looking for corporate reporting assistance? What are their biggest challenges right now, and what are some of the tools that they can use to really overcome some of those challenges?

Blythe Clark:

With reporting, the challenge is the breadth of different stakeholders with interest in ESG information. So we have, on the corporate side, stakeholders who are more interested in what I would term CSR, corporate social responsibility. So broader community engagement, employees, a much wider stake of different users of information. And then we have investors, who are typically interested in financially material information. In order to ensure that a company's disclosures meet the needs of investors, I typically recommend use of standards. And the standards that we often see and find the most useful are the recommendations of the Taskforce on Climate-related Financial Disclosure and Sustainability Accounting Standards Board, or SASB, as it's more commonly known.

Keesa Schreane:

Okay. So I'm glad that you spoke through those acronyms. SASB and TCFD, as they're called. Also, I'm hearing a bit about private equity. ESG and private equity. Could you share with us, have you advised? And if so, what are some of the big challenges and solutions that you're seeing with private equity?

Blythe Clark:

Yeah, absolutely. So within the private markets, private equity, private debt, infrastructure, real estate, we are seeing an interest in ESG. ESG has been around and has been applied in the public markets, so stocks and bonds, arguably for a little longer. Within private equity, there's a lot of opportunity to apply ESG integration in the investment process. It's a bit of a double-edged sword in that it's more challenging, because as an asset manager in private equity, you own the company and you have boots on the ground, so to speak. So it's a little more hands-on than if you own a stock or a bond. So the challenge is that it's more hands-on. The benefit, I would say, what makes it potentially a bit easier, the flip side is that a private equity investor will typically have more control over their investments than a manager who holds a stake in a publicly traded firm.

Keesa Schreane:

And in terms of, again, outcome, what is an outcome dealt with, or what has been the desired success metric in terms of private equity, specifically? Where has a private equity investor wanted to get to?

Blythe Clark:

We see a lot of private equity investors becoming signatories to the UN Principles for Responsible Investment. Becoming a UNPRI signatory requires annual reporting and assessment in which investors are given a score. And scoring well on that assessment can be challenging for smaller asset managers, and often private equity managers are smaller than, say, the giant public equity managers in the US and globally. So we work with a number of clients on UNPRI assessment preparedness in the private market. So private equity, private debt, infrastructure, real estate.

Keesa Schreane:

Got it. Perfect. Perfect. So let's bring us back to where we started. Could you summarize the issues at the heart of the Attorneys General concerns around ESG investing right now?

Blythe Clark:

Absolutely. It really comes down to differentiating between values and valuation in the context of fiduciary duty. We have one side arguing that considering environmental, social and governance issues violates fiduciary duty, while the other side feels that considering these issues is an important part of fiduciary duty. At the bottom of it, we have a disagreement about what exactly is meant by ESG investing. So those who oppose it and sometimes refer to it as woke capital believe it's values-based. It can be, but it's not by definition. In reality, where ESG issues have financially material impact on the value of an investment, a manager has a responsibility to consider them. Thus, as long as we have a lens of financial materiality, ESG investing is very much consistent with fiduciary duty in our view.

Keesa Schreane:

I know that ESG Global Advisors has a fabulous, fabulous chart, and it really outlines the different types of ESG investing. We're going to have that chart in the show notes, but I am so excited, because you are going to talk us through that chart right now. The different types and variations. There's more than one, and so that's a great starting point for education. So educate us. Take us through that chart that the audience can view from the show notes.

Blythe Clark:

Traditionally, the responsible investment spectrum has been presented as a continuum from valuation-oriented, so more traditional investments, to values-oriented. Traditional investing would be focused entirely on traditional financial factors and analysis, and thematic and impact investing are presented as the most values-oriented approach. We don't think this is correct, and we don't think the spectrum is in fact a perfect continuum. We believe that there is overlap, and that thematic and impact investing don't, by definition, need to sacrifice market level returns or be values-driven. We would argue that the only truly values-focused investment strategy would be screening, or more specifically excluding a specific sector or company for non-financial reasons. For example, excluding tobacco from a portfolio. And so we've tried to present this with a new responsible investment spectrum.

Keesa Schreane:

Okay, so let's go through. If we have a center and then we have either end, how would we look at that center, and then how would we look at either end of the spectrum?

Blythe Clark:

So at one end we would have traditional investment, which would rely on financial factors only. On the opposing end, we would have the most values-oriented approach, which would be screening, so exclusion of particular sectors. And in the middle we would have thematic and impact investing, which can be focused on returns, can be valuation-focused, while still employing a thematic ESG approach. Or could also potentially be values-affected, I should say.

Keesa Schreane:

Okay. So in looking at both ends of the spectrum, you talked a little earlier about the different types of frameworks and standards. I'm assuming that if we're looking for the more financially material item, we would look at having a SASB approach. If we're looking more at the impact side, we would look at having a GRI approach. Is that the case, or would you look at that a different way in terms of how to approach this?

Blythe Clark:

The various standards can be used across the spectrum, and I think it really gets down to how they are used. SASB can be utilized within a values-focused approach. However, it does apply a materiality lens. TCFD and SASB are based on financial materiality.

Keesa Schreane:

Got it. Whereas Global Reporting Initiative, I wanted to make sure we spoke out that acronym, GRI has more of a values in terms of various types of stakeholders, not just investors, like SASB and TCFD. So talk-

Blythe Clark:

Yes. Yeah, we would agree. It's a broader stakeholder. There's a broader focus, versus the more narrow materiality lens employed by SASB and TCFD.

Keesa Schreane:

Okay. So if you are working with consulting a firm that really wants to focus on, "Hey, we really need to speak directly to our investors," we would say, "Okay, SASB or TCFD." Versus, "We have a very broad group of stakeholders, NGOs, unions, other areas," we might look at GRI.

Blythe Clark:

Absolutely. And the majority of the clients I work with have a fiduciary duty, and so we typically work with SASB and TCFD.

Keesa Schreane:

Okay. In terms of educating people who have very strong views and opinions on responsible investing and whether or not it should exist in certain portfolios, asset owners, et cetera, what would be the best way to educate people across the board on how to look at responsible investing in its truest form, to really understand the differences and the nuances?

Blythe Clark:

That's a really great question. It can be really challenging, because what we encounter is that many people are using the same terms to describe different things. For example, conflating ESG investing with socially responsible investing. So ESG investing, taking a materiality lens, versus socially responsible investing, taking a values-based lens. Or SRI is the acronym we often see for socially responsible investing.

I generally recommend that people seek out reputable sources. And the ones that we rely on most frequently are the recommendations of the Taskforce on Climate-related Financial Disclosure and the various materials provided by the Sustainability Accounting Standards Board. Both have a focus on materiality and thus don't have an ideological agenda.

Keesa Schreane:

Have you seen any instances where there has been a successful meeting of the minds in terms of bringing together either side, so those who see responsible investing as just one category versus those who have seen variations and who can speak to the different types? Has there been a successful union of the two different ideologies coming together?

Blythe Clark:

The gulf is pretty large, and so I can't say I've seen a true meeting of the minds. But despite the political discourse around ESG right now, I recently attended a responsible investment conference in Chicago, and my takeaway was that despite what we're hearing from certain states, many asset owners, small and large, still feel that the integration of financially material ESG factors is extremely important and will continue to be an expectation they have for their external managers.

Keesa Schreane:

And so in terms of, again, extending this knowledge out, what are your thoughts about how retail investors and individuals who are not in the sustainable finance space, what's the best way to ensure that this information gets out to them?

Blythe Clark:

I think again, building consensus within the industry on these definitions. And this is what we're seeking to do with the visual we've produced, is to build consensus around what are we actually talking about when we say ESG investment? What are we actually talking about when we say values-driven? What does impact investing really mean?

Keesa Schreane:

And how successful have you been in doing that? You're saying that this visual, you're looking to drive that engagement. Have you won over any of the folks who've had ideas around other areas? Have they said, "Okay, I see the light now. I see what you're communicating." How has that happened? Have you won people over, or is there still a challenge?

Blythe Clark:

I think it's still a challenge, but things are progressing. We see boards of directors, both at investors and companies, increasingly acknowledge the importance of these issues, both from an investor and financial standpoint and from a stakeholder standpoint within their own organizations. So the tide is turning, I think.

Keesa Schreane:

Is it important for your team to be more political in terms of getting into specific policy discussions to ensure that on the political front this is recognized as well?

Blythe Clark:

No, we don't, as a matter of practice, take political positions. It goes back to our approach of being a pragmatist. We want to meet clients where they're at and meet their needs, and so we wouldn't want to take a political position. However, we do believe that to the extent they are financially material, it is really important for investors to take into account ES and G factors.

Keesa Schreane:

So let's look at the different types of investors out there. We'll start with private equity. If I am in private equity, which side of that spectrum should I be focused on? Or what are the use cases for the various sides of the spectrums for someone in private equity?

Blythe Clark:

So within private equity, I think that that investment approach and asset class can exist anywhere on that spectrum. It can be a traditional financial focus taking into account E, S and G factors only so far as they are material. However, within private equity, because there's often a more generally thematic approach, so a type of company that the investor seeks to invest in, it's typically a smaller or more concentrated portfolio. There are significant opportunities for impact investment and thematic investment related to ESG within that asset class.

Keesa Schreane:

Now what are the challenges? So there's some opportunities; what are the challenges there? You spoke earlier about the challenges that exist in terms of private equity being more hands-on and the benefit being having more control. In terms of using these different types of filters, if you will, are there specific challenges and opportunities per each filter?

Blythe Clark:

So I'll use climate as an example of some of the challenges a private equity investor faces. When it comes to measuring the carbon footprint of a portfolio in the public markets, so say a public stock portfolio, it can be as simple as purchasing a dataset, or uploading a portfolio to an online software service that subsequently spits out a detailed analysis of the portfolio's carbon footprint. When it comes to private equity, the businesses are typically smaller and they're privately owned, so they're generally not disclosing and maybe not even measuring a business's carbon footprint. So when it comes to measuring the carbon footprint of a private equity portfolio, the investor doesn't have as many tools at their disposal. On the flip side, they have more control. So what they can do is have a carbon inventory completed on each of their portfolio companies, or port-cos.

Keesa Schreane:

Okay, great. Great. And we haven't talked a lot about fixed income. And so I'm wondering again, if we're looking at the spectrum, is there a certain tool or filter that someone in the fixed income area would look to operate with most?

Blythe Clark:

That's a great question. Within the public markets, fixed income investors have greater challenges than equity investors because they don't have as much influence. They don't vote proxies, so they have one less avenue with which to influence management through engagement. So that is a challenge for fixed income investors, though we increasingly see investors engaging with the companies they hold and discussing both their equity positions and their debt positions when they in fact hold both. So that's an opportunity there on the public markets. Well, both a challenge and an opportunity.

And on the private markets, we see private debt operate more similarly to private equity. There are the same challenges around the smaller companies. The port-cos are typically smaller and have fewer resources than large public companies. It's more difficult to, say, complete a portfolio carbon footprint, a measurement when it comes to private debt. Even moreso than private equity, a private debt investor will encounter challenges in that they don't own the company, so they don't have as much control as a private equity investor would.

Keesa Schreane:

And so in terms of private equity as well as debt, is there a need to think through how to communicate, even though it's challenging, how to communicate these issues? With public companies, for example, you have sustainability reports, you have [inaudible 00:19:04], et cetera. If you are on the private side, what is the recommendation?

Blythe Clark:

Yeah, we're absolutely seeing a greater demand for reporting and disclosure from private markets investors. The Institutional Limited Partners Association, or ILPA, has put out some useful resources that we typically recommend our clients in the private market space refer to when considering what to include in their disclosures. ILPA has resources around diversity, and also around ... they've changed the name recently. I believe it's now called the ESG Data Convergence Initiative. But it seeks to build consistency around what types of ESG metrics are disclosed by private market investors regarding their investments, the portfolio level and port-co level data.

Keesa Schreane:

Okay. And getting into the public markets. I know that we have the graphic here, the visual here. I'm assuming every angle, every filter can be utilized by public market companies.

Blythe Clark:

Absolutely. So we do see every approach employed within the public markets, though impact investing is more challenging in the public markets in that as a stockholder, you'll typically have a small stake. You won't have any control. It's harder to draw that line between ownership and impact with a small holding of a company.

Keesa Schreane:

We were actually just talking to the President of a community development financial institution, Amir Kirkwood, and he was talking about leveraging our CDFIs being a true source of true impact investing there. Do you see other tools similar to CDFIs that can really be true 100% pure impact investing tools?

Blythe Clark:

We often see the UN sustainable development goals used as an important tool to measure and define impact within impact investment portfolios. So that would be an important tool. But I would agree that the types of asset owners that are really driving the demand for impact investments are community foundations, other foundations and endowments.

Keesa Schreane:

So Blythe, tell us something that you're really excited about right now, some work that you're seeing happening, whether it's in the regulation front with regulatory issues, whether it's more in the business community, or even in the investment community. What's coming down the pipeline that you're really excited about?

Blythe Clark:

I'm really excited about all of the opportunities related to the evolution of ESG in the private markets, as we've been talking about. Like we had said, ESG has been around in the public markets for quite a while now, and we're really seeing an increase in interest from asset owners and other stakeholders through things like the ESG Data Convergence Initiative from the Institutional Limited Partners Association.

Keesa Schreane:

Great. And also, tell us something that we don't know. So something that you might have been discussing, this can be public knowledge, but something that we don't know, a way that's connected the dots in a way that really hasn't been done before, or just something that's new that you see percolating that has to do with our market.

Blythe Clark:

Absolutely. So we'd spoken earlier about the lack of consensus around terminology. One of the things we are seeing happen is regulatory approaches in other jurisdictions affecting investors outside of that jurisdiction. We recently published a thought leadership piece on this called Regulation Without Borders. And what we've identified is that, for example, Europe is in many ways ahead of North America when it comes to standardization and regulation around ESG disclosures. While professional investors in Canada and the US are technically not subject to the regulations in Europe, which are called the ... it's a bit of a mouthful, but the Sustainable Finance Disclosure Requirements, or SFDR. We find that while not explicitly subject to these rules, they are often affected, for two reasons. One, if they market a fund into Europe, they will be required to make those disclosures. Two, if they manage money for a client that is subject to those recommendations, that client will most likely require from them the information in order to make these disclosures. And in this way, we see these regulations from outside of our borders impacting investors locally. And so that's something we're watching closely to think about what types of regulations are we going to see in the future? What are the expectations for investors, and how will they develop?

Keesa Schreane:

Great. And speaking of that too, for our partners and listeners who are in the Asia region, maybe the Middle East, you mentioned Europe, EU; are you seeing that same thing happening where there are some areas ... I know with Japan and other areas, they're looking to incorporate some of this more as well. What are you seeing from Asia?

Blythe Clark:

Absolutely, yeah. So we are seeing particularly an increased interest in ESG issues in the Middle Eastern markets. We have a number of clients we work with in that region. And as those economies diversify away from resources, we expect this to continue.

Keesa Schreane:

And I've heard that as well. Why is there such an emphasis right now in the Middle East?

Blythe Clark:

That's a great question. There's a lot of investments there. There's a lot of money to be invested, and therefore a lot of opportunities and a lot of new asset managers, new and growing asset managers. And they are subject to the same pressures. Capital is global, so they have the same pressures, I believe. In some ways it's different, depending on who their client bases are, but within that region, they wouldn't be immune to the same sort of ... a rising tide lifts all boats. And as expectations and best practices evolve elsewhere, other regions are influenced.

Keesa Schreane:

Well, this has been a fantastic conversation, Blythe. Everything from talking about just the emergence of woke ESG, woke capitalism, to talking about the wonderful visual that you have that really explains the different variations and various approaches to private markets as well as public markets.

One last question. I'm wondering about your work in terms of weapons exclusion and what we've seen over the last couple of years, particularly since the war has started. Do we see a different approach to weapons exclusions now than we did pre-war, or do we see the same sort of approaches?

Blythe Clark:

That's a great question, Keesa. One of the things that we've noticed over the past year or two, since the invasion of Ukraine, is really shifting attitudes around exclusion of weapons from investment portfolios. So after tobacco, weapons, I would say, are probably one of the most common exclusion that an asset owner will forbid, in effect, from being held in their portfolios, and place constraints on their investment managers, saying, "No positions in companies deriving more than, say, 10% of their revenues from the sale of weapons." Since the invasion of Ukraine, we've seen attitudes shift in that instead of being viewed in exclusively a negative light, weapons are potentially being viewed more positively in that they are a necessity for counteracting aggression from certain states.

Keesa Schreane:

So with the invasion of Ukraine, we are seeing that weapons might be something that investors who formally would not look at them in their portfolios are seeing them from a different perspective, and are looking at different perspectives, and maybe they're having changes of heart.

Blythe Clark:

Absolutely, yeah. A definite shift in attitudes towards weapons exclusions.

Keesa Schreane:

Well, this has been a fantastic conversation. Blythe Clarke of ESG Global Advisors, thank you so much for your time and for sharing with us.

Blythe Clark:

It's my pleasure, Keesa. Great to be here.

Keesa Schreane:

Thanks for joining us on today's episode of Climate. Money. Work. Please follow the show wherever you're listening right now. If you have any questions, feedback, or pitches, please get in touch with the team at cmw@shrugcontent.com. Again, that's cmw@shrug, S-H-R-U-G, content.com. Now, you can learn more about the show at keesaschreane.com/podcast. You can find me on LinkedIn, Twitter, and Instagram. I'm Keesa Schreane and thank you for listening. Be well.